Deferred Maintenance Is a Balance-Sheet Liability—Not Just a Facilities Issue

Deferred maintenance is often discussed as an operational challenge.

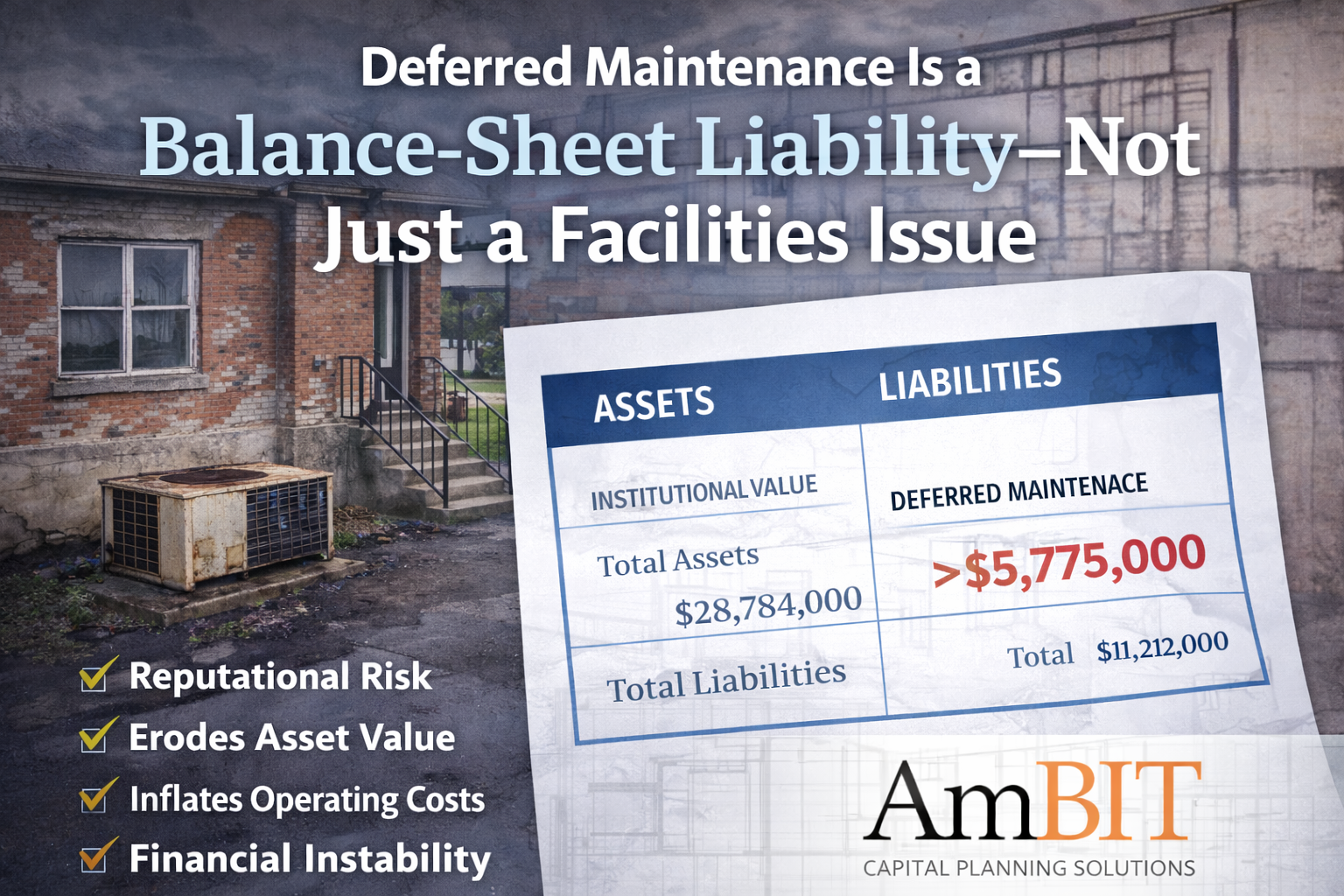

But in reality, it’s a financial one.

When renewal projects are postponed year after year, the impact doesn’t stay in the boiler room or on the roof. It migrates quietly onto the balance sheet.

Deferred maintenance:

• Erodes the value of institutional assets

• Increases long-term operating costs

• Raises the probability of disruptive failures

• Compounds future capital requirements

• Signals potential instability to boards, lenders, and donors

Physical assets are often one of the largest line items an institution owns. When their condition declines, so does the strength of the institution’s financial position.

Yet many schools lack a clear, quantified understanding of:

- The total magnitude of deferred maintenance

- The risk exposure associated with specific systems

- The timeline of probable failures

- The long-term cost of continued deferral

Without objective data, conversations become anecdotal. Decisions become reactive. And risk quietly accumulates.

Forward-thinking institutions are reframing facilities discussions in financial and risk-management terms.

They are asking:

✔ What is our true deferred maintenance liability?

✔ Which systems represent the highest financial exposure?

✔ How does this impact borrowing capacity or donor confidence?

✔ What phased strategy reduces long-term risk?

At AmBIT, we help institutions translate facility condition into defensible financial insight—so boards and leadership teams can make informed decisions grounded in data, not assumptions.

Deferred maintenance isn’t just about aging buildings.

It’s about financial stewardship.

White Paper:

Deferred Maintenance Is a Balance-Sheet Liability—Not Just a Facilities Issue

Executive Summary

For small universities, community colleges, private high schools, and preparatory schools, deferred maintenance is often viewed as an operational concern—something for the facilities department to manage as budgets allow.

In reality, deferred maintenance is a financial liability.

Unaddressed capital renewal needs erode asset value, increase operating costs, introduce institutional risk, and influence how boards, lenders, donors, and accreditors evaluate the organization’s long-term stability.

This paper reframes deferred maintenance not as a technical issue—but as a balance-sheet and risk-management issue requiring executive-level attention and structured planning.

Physical Assets Are Financial Assets

For most educational institutions, buildings and site infrastructure represent one of the largest categories of owned assets.

Academic buildings

Residence halls

Athletic facilities

Utility infrastructure

Site improvements

These assets support revenue generation, student experience, donor engagement, and institutional reputation.

When their condition declines, the institution’s financial strength declines with them.

Deferred maintenance is not merely “aging infrastructure.”

It is the gradual degradation of capital assets that directly impacts institutional value.

The Hidden Financial Impacts of Deferral

Deferred maintenance quietly produces measurable financial consequences:

1. Erosion of Asset Value

As systems operate beyond intended service life, replacement costs rise and functional value decreases. Deferred renewal effectively accelerates asset depreciation.

2. Increased Operating Costs

Older mechanical systems consume more energy. Emergency repairs carry premium pricing. Staff time shifts from preventive maintenance to crisis response.

3. Compounded Capital Exposure

Deferral rarely eliminates cost—it escalates it. Minor roof repairs can become structural damage. Equipment failures can impact multiple systems simultaneously.

4. Reputational Risk

Boards, lenders, and donors increasingly evaluate institutional health through physical condition and capital planning discipline. Visible deterioration signals instability.

Deferred maintenance accumulates quietly—until it becomes visible in financial performance and stakeholder confidence.

Why Many Institutions Underestimate the Liability

In many cases, leadership lacks clear visibility into:

- The total magnitude of deferred maintenance

- The risk profile of individual systems

- The timeline of probable failures

- The projected cost escalation if action is delayed

Without objective data, conversations rely on anecdotal input or isolated incidents.

Facilities issues are discussed in operational terms.

Budget discussions are conducted separately.

The connection between physical condition and financial exposure remains under-quantified.

As a result, deferred maintenance grows—unseen on formal financial statements but very real in institutional risk.

Deferred Maintenance as a Risk Management Issue

Forward-looking institutions are reframing the conversation.

Instead of asking:

“What can we afford to fix this year?”

They are asking:

- What is our total capital exposure?

- Which systems represent the highest financial risk?

- What failure scenarios would disrupt operations or enrollment?

- How does this affect borrowing capacity or donor confidence?

This shift moves facilities planning from maintenance management to enterprise risk management.

It aligns capital stewardship with fiduciary responsibility.

The Role of Objective Data

Strategic decisions require defensible information.

Comprehensive facility condition assessments provide:

- Verified system condition ratings

- Remaining useful life projections

- Order-of-magnitude cost forecasting

- Risk-based prioritization models

- Multi-year capital projections

With reliable data, leadership can:

- Quantify deferred maintenance liability

- Align capital planning with financial capacity

- Present clear, structured plans to trustees

- Reduce institutional risk exposure

Data transforms facilities from a reactive cost center into a strategic planning tool.

Governance, Stewardship, and Institutional Confidence

Trustees and executive leaders carry fiduciary responsibility for institutional assets.

Demonstrating structured capital planning:

- Reinforces fiscal discipline

- Enhances board confidence

- Supports bond and financing discussions

- Strengthens donor trust

- Signals institutional stability to external stakeholders

Institutions that proactively quantify and address deferred maintenance communicate something powerful:

We understand our risks.

We have a plan.

We are stewarding our assets responsibly.

How AmBIT Supports Leadership Teams

AmBIT works with small and mid-sized educational institutions to translate facility condition into actionable financial insight.

Our approach focuses on:

- Objective, third-party facility condition assessments

- Risk-priority scoring and exposure modeling

- Multi-year capital forecasting aligned with funding reality

- Executive-ready reporting that supports board-level discussions

We help institutions move from anecdotal facilities conversations to structured, defensible financial planning.

Conclusion

Deferred maintenance is not simply a facilities backlog.

It is a growing financial liability that influences asset value, operating cost, risk exposure, and institutional confidence.

Educational institutions operating under enrollment and budget pressure cannot afford unmanaged capital uncertainty.

By quantifying deferred maintenance and aligning it with strategic financial planning, leadership transforms a hidden liability into a managed risk.

In today’s environment, facilities stewardship is financial stewardship.

Written by

AmBIT Author